# Homeowner's Insurance (HOI) Guide

Insurance is a contract between the property owner and an insurance company, where the insurer agrees to provide financial compensation in case of specified events or damages.

Homeowner’s insurance (HOI) documents can be in the form of HOI policies, HOI binders, coverage declarations page, certificate of insurance, evidence of insurance, etc. They are provided by an insurance company to prove that an individual or entity has an active insurance policy in place.

The lender will require proof of insurance before closing the loan. The borrower is responsible for obtaining and maintaining the required insurance policies.

In addition to proof of insurance, the lender may also require the borrower to name them as the "mortgagee" or "loss payee" on the insurance policy. This means that in the event of a covered loss, the insurance company will include the lender as a beneficiary and ensure that any insurance proceeds are used to repair or rebuild the property.

## Reviewing the HOI & Updating Encompass

When reviewing an HOI policy for the subject property, keep in mind the following steps:

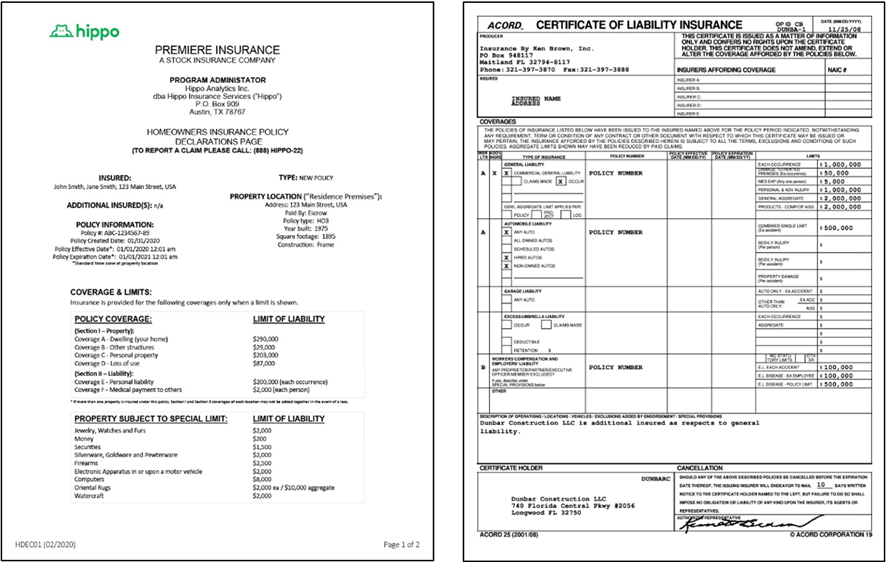

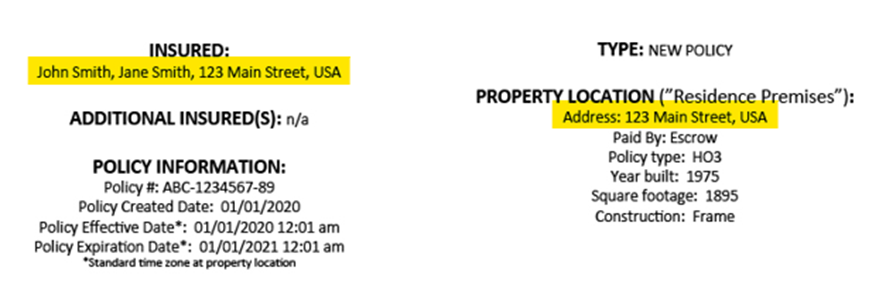

1. Identify the proposed insured people and address. The insured people must match the borrowers on file. The insured address must exactly match the subject property address on file.

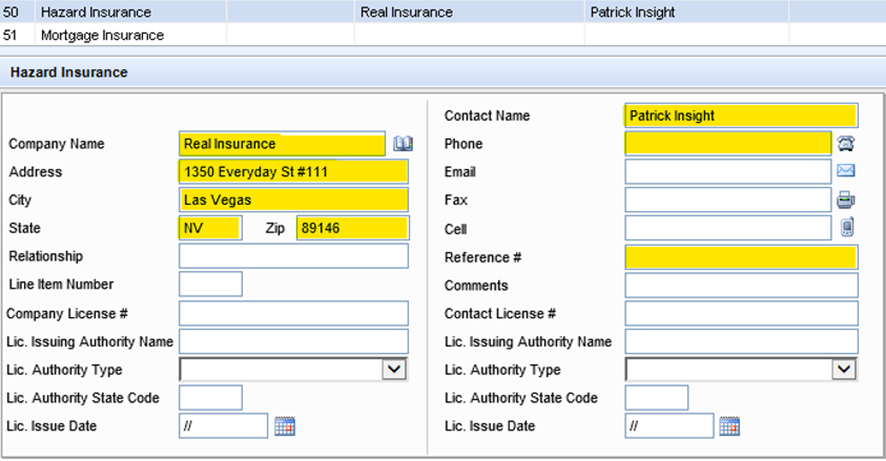

2. Locate the Hazard Insurance company information, the policy number, and the insurance agent information and add the information to the Hazard Insurance file contact in Encompass. Go to Tools > File Contacts and search for the Hazard Insurance line. Add the policy number to the Reference # field.

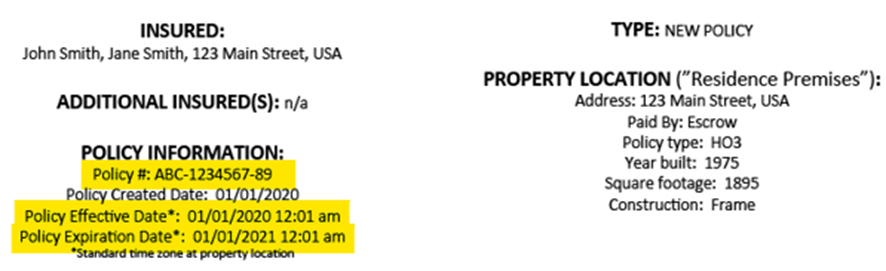

3. Find the policy start date or effective date.

* The effective date cannot be after the closing date.

* The effective date can be earlier than the closing date, as long as the effective date falls within the same month as the closing date.

* If the closing date is within the first 5 days of the month (e.g., January 1st–5th), the effective date can fall within the previous month. E.g., a loan closing on January 2nd can have a homeowner’s insurance with an effective date falling in December or of January 1st or 2nd.

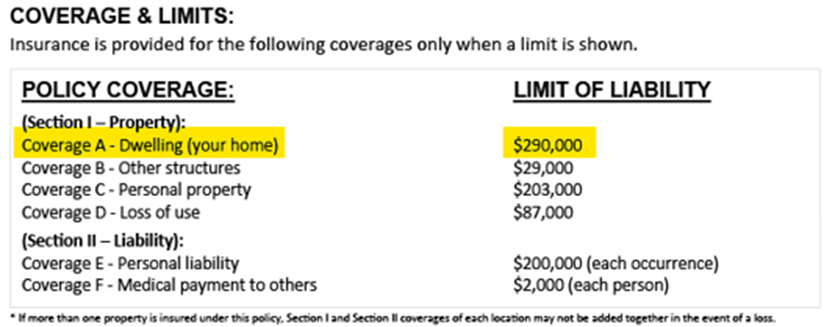

4. Locate the dwelling coverage. Dwelling coverage helps insured people pay for the rebuilding or repair of the home structure if it’s damaged by a covered hazard. Dwelling coverage can usually be found in Section I – Property. The dwelling coverage limit must match or exceed the loan amount for the policy to be valid.

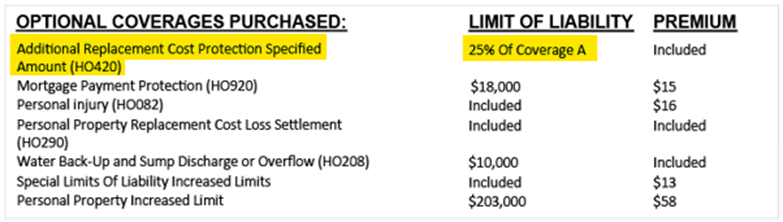

* If the Dwelling coverage limit is smaller than the loan amount, search for the Additional Replacement Cost coverage. (Not all policies have this.) You can use the sum of the Dwelling coverage limit and the Additional Replacement Cost coverage limit to compare against the loan amount to confirm the policy is valid.\

\&#xNAN;*E.g. Our borrower has a loan amount of $350,000 and the Dwelling coverage limit is only $290,000. Normally, this would mean the policy is not valid and a new one with appropriate Dwelling coverage limit must be obtained. However, the policy includes Additional Replacement Cost coverage limit for 25% of the Dwelling coverage ($72,500). While the Dwelling coverage limit alone does not match or exceed the loan amount, the Dwelling coverage limit plus the Additional Replacement Cost coverage limit do (for a total coverage limit of $362,500). Therefore, this policy is valid, and a new policy is not needed.*

* If neither the Dwelling coverage limit nor the sum of the Dwelling coverage limit and the Additional Replacement Cost coverage limit match or exceed the loan amount, a Replacement Cost Estimator (RCE) can be obtained from the insurer. The RCE serves as proof that the coverage in the policy is sufficient to rebuild of repair the home structure if it’s damaged by a covered hazard.

5. Locate the mortgagee, loss payee, or additional insured. On policies for the subject property, this section must list the company’s loss payee clause shown below.

|

Panorama Mortgage Group, LLC

ISAOA/ATIMA

6623 Las Vegas Blvd. South, Ste F-200

Las Vegas, NV 89119

|

| ----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------- |

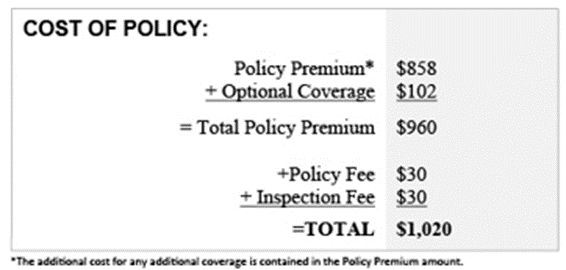

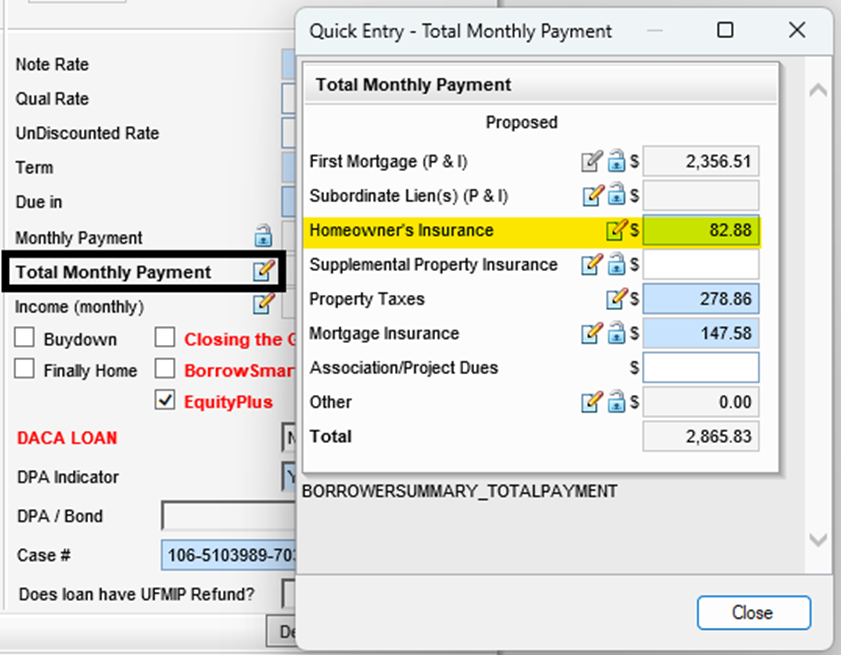

6. Locate the policy amount or premium amount. This always represents an annual amount. Calculate the monthly amount and add it to the Homeowner’s Insurance line of the Total Monthly Payment in Encompass. Go to Forms > Borrower Summary || Enhanced, scroll down to the Transaction Details section, locate the Total Monthly Payment line, and click the Edit icon to open the Total Monthly Payment window. Add the monthly insurance amount to the Homeowner’s Insurance line.